Simple Fibonacci Retracement Strategy This strategy uses Fibonacci retracement to identify key levels in the market and helps traders find good entry and exit points. By understanding and using this strategy, traders can improve their trading decisions and increase their chances of success in the market.

This strategy, called the "Simple Fibonacci Retracement Strategy," is designed to help traders identify potential entry and exit points in the market based on Fibonacci retracement levels. The code is written in Pine Script and runs on the TradingView platform.

Overall Function

The strategy uses Fibonacci retracement levels to identify potential support and resistance levels in the market. This helps traders find good entry and exit points for trades, as well as set stop-loss and take-profit levels to minimize risk and maximize gains.

Main Components of the Code

1. Input Parameters

Lookback Period: The number of bars used to identify the highest high and lowest low.

Fibonacci Direction: The choice of whether Fibonacci levels are calculated from top to bottom or bottom to top.

Fibonacci Levels: Specific Fibonacci levels (23.6%, 38.2%, 50%, 61.8%) used to identify important price levels.

Take Profit and Stop Loss: The number of pips used to set take profit and stop loss levels.

2. Identification of Highest and Lowest Points

The code uses the lookback period to find the highest high (highestHigh) and the lowest low (lowestLow). These levels form the basis for calculating the Fibonacci levels.

3. Calculation of Fibonacci Levels

Based on the direction chosen by the user, the code calculates the various Fibonacci levels (0%, 23.6%, 38.2%, 50%, 61.8%, 100%).

4. Trading Logic

Long Signal: Generated when the price crosses above the 61.8% Fibonacci level from bottom to top.

Short Signal: Generated when the price crosses below the 38.2% Fibonacci level from top to bottom.

When a long or short signal is generated, the strategy opens a position and sets take profit and stop loss levels based on the input parameters.

5. Visualization

The strategy plots the Fibonacci levels on the chart to provide a visual representation of the calculated levels. This helps traders see where the levels are in relation to the current price.

6. Alerts

The code also has functionality to create alerts (commented out), which can notify traders of buy or sell signals.

How to Use the Strategy

Configure Parameters: Adjust the lookback period, Fibonacci direction, and levels for take profit and stop loss to your preferences.

View the Chart: The Fibonacci levels will be plotted on the chart, providing a visual overview of potential support and resistance levels.

Trade Signals: Follow the generated buy and sell signals. Set your parameters in settings and adjust according to the generated buy and sell signals in the strategy tester. The strategy will automatically set your take profit and stop loss levels.

Evaluation and Adjustment: Monitor the performance of the strategy and make adjustments as needed to optimize the results.

Norwegian

Denne strategien, kalt "Simple Fibonacci Retracement Strategy", er designet for å hjelpe tradere med å identifisere mulige inngangs- og utgangspunkter i markedet basert på Fibonacci-retracementnivåer. Koden er skrevet i Pine Script og kjøres på TradingView-plattformen.

Overordnet Funksjon

Strategien bruker Fibonacci-retracementnivåer for å identifisere potensielle støtte- og motstandsnivåer i markedet. Dette hjelper tradere med å finne gode inngangs- og utgangspunkter for handler, samt å sette stop-loss og take-profit nivåer for å minimere risiko og maksimere gevinster.

Hovedkomponenter i Koden

1. Input Parametere

Lookback Period: Antall barer som brukes til å identifisere høyeste høydepunkt og laveste lavpunkt.

Fibonacci Direction: Valg om Fibonacci-nivåene skal beregnes fra topp til bunn eller bunn til topp.

Fibonacci Levels: Spesifikke Fibonacci-nivåer (23.6%, 38.2%, 50%, 61.8%) som brukes til å identifisere viktige prisnivåer.

Take Profit og Stop Loss: Antall pips som brukes til å sette take profit og stop loss nivåer.

2. Identifikasjon av Høyeste og Laveste Punkt

Koden bruker lookback perioden for å finne det høyeste høydepunktet (highestHigh) og det laveste lavpunktet (lowestLow). Disse nivåene er grunnlaget for å beregne Fibonacci-nivåene.

3. Beregning av Fibonacci-nivåer

Basert på retningen valgt av brukeren, beregner koden de forskjellige Fibonacci-nivåene (0%, 23.6%, 38.2%, 50%, 61.8%, 100%).

4. Handelslogikk

Long Signal: Genereres når prisen krysser over 61.8% Fibonacci-nivået fra bunn til topp.

Short Signal: Genereres når prisen krysser under 38.2% Fibonacci-nivået fra topp til bunn.

Når et long eller short signal genereres, åpner strategien en posisjon og setter take profit og stop loss nivåer basert på inputparametrene.

5. Visualisering

Strategien plottet Fibonacci-nivåene på chartet for å gi en visuell representasjon av de beregnede nivåene. Dette hjelper tradere med å se hvor nivåene er i forhold til den nåværende prisen.

6. Varsler

Koden har også funksjonalitet for å lage varsler (kommentert ut), som kan varsle tradere om kjøps- eller salgssignaler.

Slik Bruker Du Strategien

Konfigurer Parametere: Juster lookback perioden, Fibonacci-retningen, og nivåene for take profit og stop loss til dine preferanser.

Se på Chartet: Fibonacci-nivåene vil bli plottet på chartet, noe som gir deg en visuell oversikt over potensielle støtte- og motstandsnivåer.

Handle Signaler: Sett dine parametere i innstillinger og juster etter genererte kjøps- og salgssignalene i strategy testeren. Strategien vil automatisk sette dine take profit og stop loss nivåer.

Evaluering og Justering: Overvåk ytelsen til strategien og gjør justeringer etter behov for å optimalisere resultatene.

ابحث في النصوص البرمجية عن "the strat"

Gann Swing Strategy [1 Bar - Multi Layer]Use this Strategy to Fine-tune inputs for your Gann swing strategy.

Strategy allows you to fine-tune the indicator for 1 TimeFrame at a time; cross Timeframe Input fine-tuning is done manually after exporting the chart data.

MEANINGFUL DESCRIPTION:

The Gann Swing Chart using the One-Bar type, also known as the Minor Trend Chart, is designed to follow single-bar movements in the market. It helps identify trends by tracking price movements. When the market makes a higher high than the previous bar from a low price, the One-Bar trend line moves up, indicating a new high and establishing the previous low as a One-Bar bottom. Conversely, when the market makes a lower low than the previous bar from a high price, the One-Bar swing line moves down, marking a new low and setting the previous high as a One-Bar top. The crossing of these swing tops and bottoms indicates a change in trend direction.

HOW TO USE THE INDICATOR / Gann-swing Strategy:

The indicator shows 1, 2, and 3-bar swings. The strategy triggers a buy when the price crosses the previously determined high.

HOW TO USE THE STRATEGY:

Strategy to Fine-Tune Inputs for Your Gann Swing Strategy

This strategy allows for the fine-tuning of indicators for one timeframe at a time. Cross-timeframe input fine-tuning is done manually after exporting the chart data.

Meaningful Description:

The Gann Swing Chart using the One-Bar type, also known as the Minor Trend Chart, is designed to follow single-bar movements in the market. It helps identify trends by tracking price movements. When the market makes a higher high than the previous bar from a low price, the One-Bar trend line moves up, indicating a new high and establishing the previous low as a One-Bar bottom. Conversely, when the market makes a lower low than the previous bar from a high price, the One-Bar swing line moves down, marking a new low and setting the previous high as a One-Bar top. The crossing of these swing tops and bottoms indicates a change in trend direction.

How to Use the Indicator / Gann-Swing Strategy:

The indicator shows 1, 2, and 3-bar swings. The strategy triggers a buy when the price crosses the previously determined high.

How to Use the Strategy:

The strategy initiates a buy if the price breaks 1, 2, or 3-bar highs, or any combination thereof. Use the inputs to determine which highs or lows need to be crossed for the strategy to go long or short.

ORIGINALITY & USEFULNESS:

The One-Bar Swing Chart stands out for its simplicity and effectiveness in capturing minor market trends. Developed by meomeo105, this Gann high and low algorithm forms the basis of the strategy. I used my approach to creating strategy out of Gann swing indicator.

DETAILED DESCRIPTION:

What is a Swing Chart?

Swing charts help traders visualize price movements and identify trends by focusing on price highs and lows. They are instrumental in spotting trend reversals and continuations.

What is the One-Bar Swing Chart?

The One-Bar Swing Chart, also known as the Minor Trend Chart, follows single-bar price movements. It plots upward swings from a low price when a higher high is made, and downward swings from a high price when a lower low is made.

Key Features:

Trend Identification : Highlights minor trends by plotting swing highs and lows based on one-bar movements.

Simple Interpretation : Crossing a swing top indicates an uptrend, while crossing a swing bottom signals a downtrend.

Customizable Periods : Users can adjust the period to fine-tune the sensitivity of the swing chart to market movements.

Practical Application:

Bullish Trend : When the One-Bar Swing line moves above a previous swing top, it indicates a bullish trend.

Bearish Trend : When the One-Bar Swing line moves below a previous swing bottom, it signals a bearish trend.

Trend Reversal : Watch for crossings of swing tops and bottoms to detect potential trend reversals.

The One-Bar Swing Chart is a powerful tool for traders looking to capture and understand market trends. By following the simple rules of swing highs and lows, it provides clear and actionable insights into market direction.

Why the Strategy Uses 100% Allocation of a Portfolio:

This strategy allocates 100% of the portfolio to trading this specific pair, which does not mean 100% of all capital but 100% of the allocated trading capital for this pair. The strategy is swing-based and does not use take profit (TP) or stop losses.

MA MACD BB BackTesterOverview:

This Pine Script™ code provides a comprehensive backtesting tool that combines Moving Average (MA), Moving Average Convergence Divergence (MACD), and Bollinger Bands (BB). It is designed to help traders analyze market trends and make informed trading decisions by testing various strategies over historical data.

Key Features:

1. Customizable Indicators:

Moving Average (MA): Smooths out price data for clearer trend direction.

MACD: Measures trend momentum through MACD Line, Signal Line, and Histogram.

Bollinger Bands (BB): Identifies overbought or oversold conditions with upper and lower bands.

2. Flexible Trading Direction: Choose between long or short positions to adapt to different market conditions.

3. Risk Management: Efficiently allocate your capital with customizable position sizes.

4. Signal Generation:

Buy Signals: Triggered by crossovers for MACD, MA, and BB.

Sell Signals: Triggered by crossunders for MACD, MA, and BB.

5. Automated Trading: Automatically enter and exit trades based on signal conditions and strategy parameters.

How It Works:

1. Indicator Selection: Select your preferred indicator (MA, MACD, BB) and trading direction (Long/Short).

2. Risk Management Configuration: Set the percentage of capital to allocate per position to manage risk effectively.

3.Signal Detection: The algorithm identifies and plots buy/sell signals directly on the chart based on the chosen indicator.

4. Trade Execution: The strategy automatically enters and exits trades based on signal conditions and configured strategy parameters.

Use Cases:

- Backtesting: Evaluate the effectiveness of trading strategies using historical data to understand potential performance.

- Strategy Development: Customize and expand the strategy to incorporate additional indicators or conditions to fit specific trading styles.

ADDONS That Affect Strategy:

1. Indicator Parameters:

Adjustments to the settings of MACD (e.g., fast length, slow length), MA (e.g., length), and BB (e.g., length, multiplier) will directly impact the detection of signals and the strategy's performance.

2. Trading Direction:

Changing the trading direction (Long/Short) will alter the entry and exit conditions based on the detected signals.

3. Risk Management Settings:

Modifying the position size percentage affects capital allocation and overall risk exposure per trade.

ADDONS That Do Not Affect Strategy:

1. Visual Customizations:

Changes to the color, shape, and style of the plotted lines and signals do not impact the core functionality of the strategy but enhance visual clarity.

2. Text and Labels:

Modifying text labels for the signals (such as renaming "Buy MACD" to "MACD Buy Signal") is purely cosmetic and does not influence the strategy’s logic or outcomes.

Notes:

- Customization: The indicator is highly customizable to fit various trading styles and market conditions.

- Risk Management: Adjust position sizes and risk parameters according to your risk tolerance and account size.

- Optimization: Regularly backtest and optimize parameters to adapt to changing market dynamics for better performance.

Getting Started:

-Add the script to your chart.

-Adjust the input parameters to suit your analysis preferences.

-Observe the marked buy and sell signals on your chart to make informed trading decisions.

Momentum Alligator 4h Bitcoin StrategyOverview

The Momentum Alligator 4h Bitcoin Strategy is a trend-following trading system that operates on dual time frames. It utilizes the 1D Williams Alligator indicator to identify the prevailing major price trend and seeks trading opportunities on the 4-hour (4h) time frame when the momentum is turning up. The strategy is designed to close trades if the trend fails to develop or holding position if price continues increasing without any significant correction. Note that this strategy is specifically tailored for the 4-hour time frame.

Unique Features

2-layers market noise filtering system: Trades are only initiated in the direction of the 1D trend, determined by the Williams Alligator indicator. This higher time frame confirmation filters out minor trade signals, focusing on more substantial opportunities. At the same time, strategy has additional filter on 4h time frame with Awesome Oscillator which is showing the current price momentum.

Flexible Risk Management: The strategy exclusively opens long positions, resulting in fewer trades during bear markets. It incorporates a dynamic stop-loss mechanism, which can either follow the jaw line of the 4h Alligator or a user-defined fixed stop-loss. This flexibility helps manage risk and avoid non-trending markets.

Methodology

The strategy initiates a long position when the d-line of Stochastic RSI crosses up it's k-line. It means that there is a high probability that price momentum reversed from down to up. To avoid overtrading in potentially choppy markets, it skips the next two trades following a winning trade, anticipating sideways movement after a significant price surge.

This strategy has two layers trades filtering system: 4h and 1D time frames. The first one is awesome oscillator. It shall be increasing and value has to be higher than it's 5-period SMA. This is an additional confirmation that long trade is opened in the direction of the current momentum. As it was mentioned above, all entry signals are validated against the 1D Williams Alligator indicator. A trade is only opened if the price is above all three lines of the 1D Alligator, ensuring alignment with the major trend.

A trade is closed if the price hits the 4h jaw line of the Alligator or reaches the user-defined stop-loss level.

Risk Management

The strategy employs a combined approach to risk management:

It allows positions to ride the trend as long as the price continues to move favorably, aiming to capture significant price movements. It features a user-defined stop-loss parameter to mitigate risks based on individual risk tolerance. By default, this stop-loss is set to a 2% drop from the entry point, but it can be adjusted according to the trader's preferences.

Justification of Methodology

This strategy leverages Stochastic RSI on 4h time frame to open long trade when momentum started reversing to the upside. On the one hand, Stochastic RSI is one of the most sensitive indicator, which allows to react fast on the potential trend reversal. On the other hand, this indicator can be too sensitive and provide a lot of false trend changing signals. To eliminate this weakness we use two-layers trades filtering system.

The first layer is the 4h Awesome oscillator. This is less sensitive momentum indicator. Usually it starts increasing when price has already passed significant distance from the actual reversal point. The strategy opens long trade only is Awesome oscillator is increasing and above it's 5-period SMA. This approach increases the probability to filter the false signals during the choppy market or if the reversal is false.

The second layer filter is the Williams Alligator indicator on 1D time frame. The 1D Alligator serves as a filter for identifying the primary trend and increases probability to avoid the trades with low potential because trading against major trend usually is more risky. It's much better to catch the trend continuation than local bounce.

Last but not least feature of this strategy is close trades condition. It uses the flexible approach. First of all, user can set up the fixed stop-loss according to his own risk-tolerance, by default this value is 2% of price movement. It restricts the potential loss at the moment when trade has just been opened. Moreover strategy utilizes the 4h Williams Alligator's jaw line to exit the trade. If price fell below it trade is closed. This approach helps to not keep open trade if trend is not developing and hold it if price continues going up.

Backtest Results:

Operating window: Date range of backtests is 2021.01.01 - 2024.05.01. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 50%

Maximum Single Position Loss: -3.04%

Maximum Single Profit: +29.67%

Net Profit: +6228.01 USDT (+62.28%)

Total Trades: 118 (24.58% win rate)

Profit Factor: 1.71

Maximum Accumulated Loss: 1527.69 USDT (-11.52%)

Average Profit per Trade: 52.78 USDT (+0.89%)

Average Trade Duration: 60 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

How to Use:

Add the script to favorites for easy access.

Apply to the 4h timeframe desired chart (optimal performance observed on the BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

Stochastic Z-Score Oscillator Strategy [TradeDots]The "Stochastic Z-Score Oscillator Strategy" represents an enhanced approach to the original "Buy Sell Strategy With Z-Score" trading strategy. Our upgraded Stochastic model incorporates an additional Stochastic Oscillator layer on top of the Z-Score statistical metrics, which bolsters the affirmation of potential price reversals.

We also revised our exit strategy to when the Z-Score revert to a level of zero. This amendment gives a much smaller drawdown, resulting in a better win-rate compared to the original version.

HOW DOES IT WORK

The strategy operates by calculating the Z-Score of the closing price for each candlestick. This allows us to evaluate how significantly the current price deviates from its typical volatility level.

The strategy first takes the scope of a rolling window, adjusted to the user's preference. This window is used to compute both the standard deviation and mean value. With these values, the strategic model finalizes the Z-Score. This determination is accomplished by subtracting the mean from the closing price and dividing the resulting value by the standard deviation.

Following this, the Stochastic Oscillator is utilized to affirm the Z-Score overbought and oversold indicators. This indicator operates within a 0 to 100 range, so a base adjustment to match the Z-Score scale is required. Post Stochastic Oscillator calculation, we recalibrate the figure to lie within the -4 to 4 range.

Finally, we compute the average of both the Stochastic Oscillator and Z-Score, signaling overpriced or underpriced conditions when the set threshold of positive or negative is breached.

APPLICATION

Firstly, it is better to identify a stable trading pair for this technique, such as two stocks with considerable correlation. This is to ensure conformance with the statistical model's assumption of a normal Gaussian distribution model. The ideal performance is theoretically situated within a sideways market devoid of skewness.

Following pair selection, the user should refine the span of the rolling window. A broader window smoothens the mean, more accurately capturing long-term market trends, while potentially enhancing volatility. This refinement results in fewer, yet precise trading signals.

Finally, the user must settle on an optimal Z-Score threshold, which essentially dictates the timing for buy/sell actions when the Z-Score exceeds with thresholds. A positive threshold signifies the price veering away from its mean, triggering a sell signal. Conversely, a negative threshold denotes the price falling below its mean, illustrating an underpriced condition that prompts a buy signal.

Within a normal distribution, a Z-Score of 1 records about 68% of occurrences centered at the mean, while a Z-Score of 2 captures approximately 95% of occurrences.

The 'cool down period' is essentially the number of bars that await before the next signal generation. This feature is employed to dodge the occurrence of multiple signals in a short period.

DEFAULT SETUP

The following is the default setup on EURAUD 1h timeframe

Rolling Window: 80

Z-Score Threshold: 2.8

Signal Cool Down Period: 5

Stochastic Length: 14

Stochastic Smooth Period: 7

Commission: 0.01%

Initial Capital: $10,000

Equity per Trade: 40%

FURTHER IMPLICATION

The Stochastic Oscillator imparts minimal impact on the current strategy. As such, it may be beneficial to adjust the weightings between the Z-Score and Stochastic Oscillator values or the scale of Stochastic Oscillator to test different performance outcomes.

Alternative momentum indicators such as Keltner Channels or RSI could also serve as robust confirmations of overbought and oversold signals when used for verification.

RISK DISCLAIMER

Trading entails substantial risk, and most day traders incur losses. All content, tools, scripts, articles, and education provided by TradeDots serve purely informational and educational purposes. Past performances are not definitive predictors of future results.

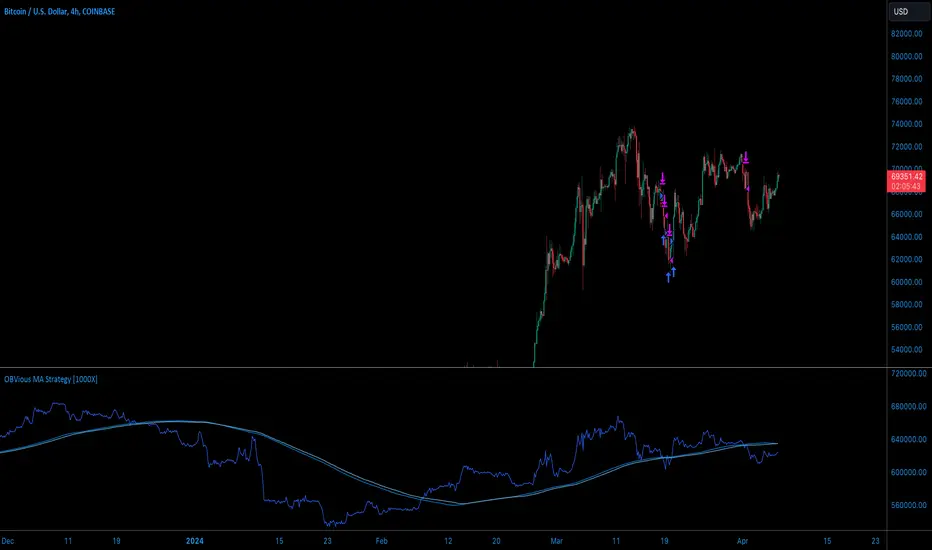

OBVious MA Strategy [1000X Trader]Exploring OBV: The OBVious MA Strategy

Are you using On Balance Volume (OBV) effectively? OBV is a gift to traders. OBV often provides a leading signal at the outset of a trend, when compression in the markets produces a surge in OBV prior to increased volatility.

This strategy demonstrates one method of utilizing OBV to your advantage. I call it the "OBVious MA Strategy ” only because it is so simple in its mechanics. This is meant to be a demonstration, not a strategy to utilize in live trading, as the primary utility of the OBVious MA indicator is as a volume confirmation filter that complements other components of a strategy. That said, I felt useful to present this indicator in isolation in this strategy to demonstrate the power it holds.

Strategy Features:

• OBV is the core signal: this strategy revolves around the On Balance Volume indicator. OBV is a straightforward indicator: it registers a value by adding total volume traded on up candles, and subtracts total volume on down candles, generating a line by connecting those values. OBV was described in 1963 by Joe Granville in his book "Granville's New Key to Stock Market Profits” in which the author argues that OBV is the most vital key to success as a trader, as volume changes are a major predictor of price changes.

• Dual Moving Averages: here we use separate moving averages for entries and exits. This allows for more granular trade management; for example, one can either extend the length of the exit MA to hold positions longer, or shorten the MA for swifter exits, independently of the entry signals.

Execution: long trades are taken when the OBV line crosses above the Long Entry Moving Average of the OBV. Long exits occur when the OBV line crosses under the Long Exit MA of the OBV. Shorts enter on a cross below the Short Entry MA, and exit on a cross above the Short Exit MA.

• Directional Trading: a direction filter can be set to "long" or "short," but not “both”, given that there is no trend filter in this strategy. When used in a bi-directional strategy with a trend filter, we add “both” to the script as a third option.

Application:

While this strategy outlines entry and exit conditions based on OBV crossovers with designated moving averages, is is, as stated, best used in conjunction with a supporting cast of confirmatory indicators (feel free to drop me a note and tell me how you've used it). It can be used to confirm entries, or you might try using it as a sole exit indicator in a strategy.

Visualization:

The strategy includes conditional plotting of the OBV MAs, which plot based on the selected trading direction. This visualization aids in understanding how OBV interacts with the set moving averages.

Further Discussion:

We all know the importance of volume; this strategy demonstrates one simple yet effective method of incorporating the OBV for volume analysis. The OBV indicator can be used in many ways - for example, we can monitor OBV trend line breaks, look for divergences, or as we do here, watch for breaks of the moving average.

Despite its simplicity, I'm unaware of any previously published cases of this method. The concept of applying MAs or EMAs to volume-based indicators like OBV is not uncommon in technical analysis, so I expect that work like this has been done before. If you know of other similar indicators or strategies, please mention in the comments.

One comparable strategy that uses EMAs of the OBV is QuantNomad’s "On Balance Volume Oscillator Strategy ", which uses a pair of EMAs on a normalized-range OBV-based oscillator. In that strategy, however, entries and exits occur on one EMA crossing the other, which places trades at distinctly different times than crossings of the OBV itself. Both are valid approaches with strength in simplicity.

Signal Filter / Connectable [Azullian]The connectable signal filter is an intricate part of an indicator system designed to help test, visualize and build strategy configurations without coding. Like all connectable indicators , it interacts through the TradingView input source, which serves as a signal connector to link indicators to each other. All connectable indicators send signal weight to the next node in the system until it reaches either a connectable signal monitor, signal filter and/or strategy.

The connectable signal filter's function has several roles in the connectable system:

• Input hub: Connect indicators or daisy-chained indicators directly to the filter, manage connections in one place

• Modification: Modify incoming signals by applying smoothing, scaling, or modifiers

• Filtering: Set the trade direction and conditions a signal must adhere to to be passed through

• Visualization: When connected, the signal filter visualizes all incoming signal weights

Let's review the separate parts of this indicator.

█ INPUTS

We've provided 3 inputs for connecting indicators or chains (1→, 2→, 3→) which are all set to 'Close' by default.

An input has several controls:

• Enable disable: Toggle the entire input on or off

• Input: Connect indicators here, choose indicators with a compatible : Signal connector.

• G - Gain: Increase or reduce the strength of the incoming signal by a factor.

█ FILTER SIGNALS

The core of the signal filter , determine a signal direction with the signal mode and determine a threshold (TH).

• ¤ - Trade direction:

○ EL: Send Enter Long signals to the strategy

○ XL: Send Exit Long signals to the strategy

○ ES: Send Enter Short signals to the strategy

○ XS: Send Exit Short signals to the strategy

• TH - Threshold: Define how much weight is needed for a signal to be accepted and passed through to the connectable strategy .

■ VISUALS

• ☼: Brightness % : Set the opacity for the signal curves

• 🡓: ES Color : Set the color for the ES: Entry Short signal

• ⭳: XS Color : Set the color for the XS: Exit Short signal

• ⌥: Plot mode : Set the plotting mode

○ Signals IN: Show all signals

○ Signals OUT: Show only scoring signals

• 🡑: EL Color : Set the color for the EL: Enter Long signal

• ⭱: XL Color : Set the color for the XL: Exit Long signal

█ USAGE OF CONNECTABLE INDICATORS

■ Connectable chaining mechanism

Connectable indicators can be connected directly to the signal monitor, signal filter or strategy , or they can be daisy chained to each other while the last indicator in the chain connects to the signal monitor, signal filter or strategy. When using a signal filter you can chain the filter to the strategy input to make your chain complete.

• Direct chaining: Connect an indicator directly to the signal monitor, signal filter or strategy through the provided inputs (→).

• Daisy chaining: Connect indicators using the indicator input (→). The first in a daisy chain should have a flow (⌥) set to 'Indicator only'. Subsequent indicators use 'Both' to pass the previous weight. The final indicator connects to the signal monitor, signal filter, or strategy.

■ Set up the signal filter with a connectable indicator and strategy

Let's connect the MACD to a connectable signal filter and a strategy :

1. Load all relevant indicators

• Load MACD / Connectable

• Load Signal filter / Connectable

• Load Strategy / Connectable

2. Signal Filter: Connect the MACD to the Signal Filter

• Open the signal filter settings

• Choose one of the three input dropdowns (1→, 2→, 3→) and choose : MACD / Connectable: Signal Connector

• Toggle the enable box before the connected input to enable the incoming signal

3. Signal Filter: Update the filter settings if needed

• The default filter mode for the trading direction is SWING, and is compatible with the default settings in the strategy and indicators.

4. Signal Filter: Update the weight threshold settings if needed

• All connectable indicators load by default with a score of 6 for each direction (EL, XL, ES, XS)

• By default, weight threshold (TH) in the signal filter is set at 5. This allows each occurrence to score, as the default score in each / Connectable indicator is 6 and thus is 1 point above the threshold. Adjust to your liking.

5. Strategy: Connect the strategy to the signal filter in the strategy settings

• Select a strategy input → and select the Signal filter: Signal connector

6. Strategy: Enable filter compatible directions

• As the default setting of the signal filter has enabled EL (Enter Long), XL (Exit Long), ES (Enter Short) and XS (Exit short), the connectable strategy will receive all compatible directions.

Now that everything is connected, you'll notice green spikes in the signal filter representing long signals, and red spikes indicating short signals. Trades will also appear on the chart, complemented by a performance overview. Your journey is just beginning: delve into different scoring mechanisms, merge diverse connectable indicators, and craft unique chains. Instantly test your results and discover the potential of your configurations. Dive deep and enjoy the process!

█ BENEFITS

• Adaptable Modular Design: Arrange indicators in diverse structures via direct or daisy chaining, allowing tailored configurations to align with your analysis approach.

• Streamlined Backtesting: Simplify the iterative process of testing and adjusting combinations, facilitating a smoother exploration of potential setups.

• Intuitive Interface: Navigate TradingView with added ease. Integrate desired indicators, adjust settings, and establish alerts without delving into complex code.

• Signal Weight Precision: Leverage granular weight allocation among signals, offering a deeper layer of customization in strategy formulation.

• Advanced Signal Filtering: Define entry and exit conditions with more clarity, granting an added layer of strategy precision.

• Clear Visual Feedback: Distinct visual signals and cues enhance the readability of charts, promoting informed decision-making.

• Standardized Defaults: Indicators are equipped with universally recognized preset settings, ensuring consistency in initial setups across different types like momentum or volatility.

• Reliability: Our indicators are meticulously developed to prevent repainting. We strictly adhere to TradingView's coding conventions, ensuring our code is both performant and clean.

█ COMPATIBLE INDICATORS

Each indicator that incorporates our open-source 'azLibConnector' library and adheres to our conventions can be effortlessly integrated and used as detailed above.

For clarity and recognition within the TradingView platform, we append the suffix ' / Connectable' to every compatible indicator.

█ COMMON MISTAKES, CLARIFICATIONS AND TIPS

• Removing an indicator from a chain: Deleting a linked indicator and confirming the "remove study tree" alert will also remove all underlying indicators in the object tree. Before removing one, disconnect the adjacent indicators and move it to the object stack's bottom.

• Point systems: The azLibConnector provides 500 points for each direction (EL: Enter long, XL: Exit long, ES: Enter short, XS: Exit short) Remember this cap when devising a point structure.

• Flow misconfiguration: In daisy chains the first indicator should always have a flow (⌥) setting of 'indicator only' while other indicator should have a flow (⌥) setting of 'both'.

• Hide attributes: As connectable indicators send through quite some information you'll notice all the arguments are taking up some screenwidth and cause some visual clutter. You can disable arguments in Chart Settings / Status line.

• Layout and abbreviations: To maintain a consistent structure, we use abbreviations for each input. While this may initially seem complex, you'll quickly become familiar with them. Each abbreviation is also explained in the inline tooltips.

• Inputs: Connecting a connectable indicator directly to the strategy delivers the raw signal without a weight threshold, meaning every signal will trigger a trade.

█ A NOTE OF GRATITUDE

Through years of exploring TradingView and Pine Script, we've drawn immense inspiration from the community's knowledge and innovation. Thank you for being a constant source of motivation and insight.

█ RISK DISCLAIMER

Azullian's content, tools, scripts, articles, and educational offerings are presented purely for educational and informational uses. Please be aware that past performance should not be considered a predictor of future results.

RSI / Connectable [Azullian]Enhance your trading approach with the modular RSI indicator, skilled in identifying market extremes. Simplify pattern visualization and signal weighting for more efficient strategy formulation.

This connectable RSI indicator is part of an indicator system designed to help test, visualize and build strategy configurations without coding. Like all connectable indicators , it interacts through the TradingView input source, which serves as a signal connector to link indicators to each other. All connectable indicators send signal weight to the next node in the system until it reaches either a connectable signal monitor, signal filter and/or strategy.

█ UNIFORM SETTINGS AND A WAY OF WORK

Although connectable indicators may have specific weight scoring conditions, they all aim to follow a standardized general approach to weight scoring settings, as outlined below.

■ Connectable indicators - Settings

• 🗲 Energy: Energy applies an ATR multiplier to the plotted shapes on the chart. A higher value plots shapes farther away from the candle, enhancing visibility.

• ☼ Brightness: Brightness determines the opacity of the shape plotted on the chart, aiding visibility. Indicator weight also influences opacity.

• → Input: Use the input setting to specify a data source for the indicator. Here you can connect the indicator to other indicators.

• ⌥ Flow: Determine where you want to receive signals from:

○ Both: Weights from this indicator and the connected indicator will apply

○ Indicator only: Only weights from this indicator will apply

○ Input only: Only weights from the connected indicator will apply

• ⥅ Weight multiplier: Multiply all weights in the entire indicator by a given factor, useful for quickly testing different indicators in a granular setup.

• ⥇ Threshold: Set a threshold to indicate the minimum amount of weight it should receive to pass it through to the next indicator.

• ⥱ Limiter: Set a hard limit to the maximum amount of weight that can be fed through the indicator.

■ Connectable indicators - Weight scoring settings

▢ Weight scoring conditions

• SM – Signal mode: Enable specific conditions for weight scoring

○ All: All signals will be scored.

○ Entries only: Only entries will score.

○ Exits only: Only exits will score.

○ Entries & exits: Both entries and exits will score.

○ Zone: Continuous scoring for each candle within the zone.

• SP – Signal period: Defines a range of candles within which a signal can score.

• SC - Signal count: Specifies the number of bars to retrospectively examine and score.

○ Single: Score for a single occurrence

○ All occurrences: Score for all occurrences

○ Single + Threshold: Score for single occurrences within the signal period (SP)

○ Every + Threshold: Score for all occurrences within the signal period (SP)

▢ Weight scoring direction

• ES: Enter Short weight

• XL: Exit long weight

• EL: Enter Long weight

• XS: Exit Short weight

▢ Weight scoring values

• Weights can hold either positive or negative scores. Positive weights enhance a particular trading direction, while negative weights diminish it.

■ Entries, exits and zone illustrated on a standard RSI indicator when the RSI is overbought.

█ RSI - INDICATOR SETTINGS

■ Main settings

• Enable/Disable Indicator: Toggle the entire indicator on or off.

• S - Source: Choose an alternative data source for the RSI calculation.

• T - Timeframe: Select an alternative timeframe for the RSI calculation.

• LE - Length: Define the number of bars or periods used in the RSI calculation.

• OB - Overbought Level: Determine the RSI value at which overbought conditions are met.

• OS - Oversold Level: Specify the RSI value at which oversold conditions are met.

■ Scoring functionality

• The RSI scores long entries when the RSI enters OS: oversold area

• The RSI scores long exits when the RSI exits OS: oversold area

• The RSI scores long zones the entire time the RSI is in OS: oversold area

• The RSI scores short entries when the RSI enters OB: overbought area

• The RSI scores short exits when the RSI exits OB: overbought area

• The RSI scores short zones the entire time the RSI is in OB: overbought area

█ PLOTTING

• Standard: Symbols (EL, XS, ES, XL) appear relative to candles based on set conditions. Their opacity and position vary with weight.

• Conditional Settings: A larger icon appears if global conditions are met. For instance, with a Threshold(⥇) of 12, Signal Period (SP) of 3, and Scoring Condition (SC) set to "EVERY", an RSI signaling over two times in 3 candles (scoring 6 each) triggers a larger icon.

█ USAGE OF CONNECTABLE INDICATORS

■ Connectable chaining mechanism

Connectable indicators can be connected directly to the signal monitor, signal filter or strategy , or they can be daisy chained to each other while the last indicator in the chain connects to the signal monitor, signal filter or strategy. When using a signal filter you can chain the filter to the strategy input to make your chain complete.

• Direct chaining: Connect an indicator directly to the signal monitor, signal filter or strategy through the provided inputs (→).

• Daisy chaining: Connect indicators using the indicator input (→). The first in a daisy chain should have a flow (⌥) set to 'Indicator only'. Subsequent indicators use 'Both' to pass the previous weight. The final indicator connects to the signal monitor, signal filter, or strategy.

■ Set up this indicator with a signal filter and strategy

The indicator provides visual cues based on signal conditions. However, its weight system is best utilized when paired with a connectable signal filter, signal monitor, or strategy .

Let's connect the RSI to a connectable signal filter and a strategy :

1. Load all relevant indicators

• Load RSI / Connectable

• Load Signal filter / Connectable

• Load Strategy / Connectable

2. Signal Filter: Connect the RSI to the Signal Filter

• Open the signal filter settings

• Choose one of the three input dropdowns (1→, 2→, 3→) and choose : RSI / Connectable: Signal Connector

• Toggle the enable box before the connected input to enable the incoming signal

3. Signal Filter: Update the filter signals settings if needed

• The default settings of the filter enable EL (Enter Long), XL (Exit Long), ES (Enter Short) and XS (Exit Short).

4. Signal Filter: Update the weight threshold settings if needed

• All connectable indicators load by default with a score of 6 for each direction (EL, XL, ES, XS)

• By default, weight threshold (TH) is set at 5. This allows each occurrence to score, as the default score in each connectable indicator is 1 point above the threshold. Adjust to your liking.

5. Strategy: Connect the strategy to the signal filter in the strategy settings

• Select a strategy input → and select the Signal filter: Signal connector

6. Strategy: Enable filter compatible directions

• Set the signal mode of the strategy to a compatible direction with the signal filter.

Now that everything is connected, you'll notice green spikes in the signal filter representing long signals, and red spikes indicating short signals. Trades will also appear on the chart, complemented by a performance overview. Your journey is just beginning: delve into different scoring mechanisms, merge diverse connectable indicators, and craft unique chains. Instantly test your results and discover the potential of your configurations. Dive deep and enjoy the process!

█ BENEFITS

• Adaptable Modular Design: Arrange indicators in diverse structures via direct or daisy chaining, allowing tailored configurations to align with your analysis approach.

• Streamlined Backtesting: Simplify the iterative process of testing and adjusting combinations, facilitating a smoother exploration of potential setups.

• Intuitive Interface: Navigate TradingView with added ease. Integrate desired indicators, adjust settings, and establish alerts without delving into complex code.

• Signal Weight Precision: Leverage granular weight allocation among signals, offering a deeper layer of customization in strategy formulation.

• Advanced Signal Filtering: Define entry and exit conditions with more clarity, granting an added layer of strategy precision.

• Clear Visual Feedback: Distinct visual signals and cues enhance the readability of charts, promoting informed decision-making.

• Standardized Defaults: Indicators are equipped with universally recognized preset settings, ensuring consistency in initial setups across different types like momentum or volatility.

• Reliability: Our indicators are meticulously developed to prevent repainting. We strictly adhere to TradingView's coding conventions, ensuring our code is both performant and clean.

█ COMPATIBLE INDICATORS

Each indicator that incorporates our open-source 'azLibConnector' library and adheres to our conventions can be effortlessly integrated and used as detailed above.

For clarity and recognition within the TradingView platform, we append the suffix ' / Connectable' to every compatible indicator.

█ COMMON MISTAKES, CLARIFICATIONS AND TIPS

• Removing an indicator from a chain: Deleting a linked indicator and confirming the "remove study tree" alert will also remove all underlying indicators in the object tree. Before removing one, disconnect the adjacent indicators and move it to the object stack's bottom.

• Point systems: The azLibConnector provides 500 points for each direction (EL: Enter long, XL: Exit long, ES: Enter short, XS: Exit short) Remember this cap when devising a point structure.

• Flow misconfiguration: In daisy chains the first indicator should always have a flow (⌥) setting of 'indicator only' while other indicator should have a flow (⌥) setting of 'both'.

• Hide attributes: As connectable indicators send through quite some information you'll notice all the arguments are taking up some screenwidth and cause some visual clutter. You can disable arguments in Chart Settings / Status line.

• Layout and abbreviations: To maintain a consistent structure, we use abbreviations for each input. While this may initially seem complex, you'll quickly become familiar with them. Each abbreviation is also explained in the inline tooltips.

• Inputs: Connecting a connectable indicator directly to the strategy delivers the raw signal without a weight threshold, meaning every signal will trigger a trade.

█ A NOTE OF GRATITUDE

Through years of exploring TradingView and Pine Script, we've drawn immense inspiration from the community's knowledge and innovation. Thank you for being a constant source of motivation and insight.

█ RISK DISCLAIMER

Azullian's content, tools, scripts, articles, and educational offerings are presented purely for educational and informational uses. Please be aware that past performance should not be considered a predictor of future results.

MA / Connectable [Azullian]Streamline trend analysis with the Moving Average indicator. Filter out market noise, aiding in the clear identification of market directions for dynamic strategy development.

This connectable moving average indicator is part of an indicator system designed to help test, visualize and build strategy configurations without coding. Like all connectable indicators , it interacts through the TradingView input source, which serves as a signal connector to link indicators to each other. All connectable indicators send signal weight to the next node in the system until it reaches either a connectable signal monitor, signal filter and/or strategy.

█ UNIFORM SETTINGS AND A WAY OF WORK

Although connectable indicators may have specific weight scoring conditions, they all aim to follow a standardized general approach to weight scoring settings, as outlined below.

■ Connectable indicators - Settings

• 🗲 Energy: Energy applies an ATR multiplier to the plotted shapes on the chart. A higher value plots shapes farther away from the candle, enhancing visibility.

• ☼ Brightness: Brightness determines the opacity of the shape plotted on the chart, aiding visibility. Indicator weight also influences opacity.

• → Input: Use the input setting to specify a data source for the indicator. Here you can connect the indicator to other indicators.

• ⌥ Flow: Determine where you want to receive signals from:

○ Both: Weights from this indicator and the connected indicator will apply

○ Indicator only: Only weights from this indicator will apply

○ Input only: Only weights from the connected indicator will apply

• ⥅ Weight multiplier: Multiply all weights in the entire indicator by a given factor, useful for quickly testing different indicators in a granular setup.

• ⥇ Threshold: Set a threshold to indicate the minimum amount of weight it should receive to pass it through to the next indicator.

• ⥱ Limiter: Set a hard limit to the maximum amount of weight that can be fed through the indicator.

■ Connectable indicators - Weight scoring settings

▢ Weight scoring conditions

• SM – Signal mode: Enable specific conditions for weight scoring

○ Start: A new trend starting will score

○ End: A trend ending will score

○ Zone: Continuous scoring for each candle between the start and the end.

• SP – Signal period: Defines a range of candles within which a signal can score.

• SC - Signal count: Specifies the number of bars to retrospectively examine and score.

○ Single: Score for a single occurrence

○ All occurrences: Score for all occurrences

○ Single + Threshold: Score for single occurrences within the signal period (SP)

○ Every + Threshold: Score for all occurrences within the signal period (SP)

▢ Weight scoring direction

• ES: Enter Short weight

• XL: Exit long weight

• EL: Enter Long weight

• XS: Exit Short weight

▢ Weight scoring values

• Weights can hold either positive or negative scores. Positive weights enhance a particular trading direction, while negative weights diminish it.

█ MA - INDICATOR SETTINGS

■ Main settings

• Enable/Disable Indicator: Toggle the entire indicator on or off.

• T - Type: Choose a type of moving average. (ALMA, EMA, HMA, RMA, SMA, SWMA, VWMA, WMA)

• L - Length: Set a period on which the moving average is calculated.

• F - Filter: Set a conditional filter for scoring:

○ Line direction: Score bullish when the trend line is going up, score bearish when the trendline is going down.

○ Line candle position: Score bullish when the candles are above the current trendline, score bearish when the candles are below the current trendline

○ Any: Score if any of the previously mentioned conditions are true

○ All: Score if all of the previously mentioned conditions are true

• S - Source: Choose an alternative data source for the Moving average calculation.

• T - Timeframe: Select an alternative timeframe for the Moving average calculation.

• C - Candletype: Choose a candletype for the alternative source.

■ Scoring functionality

• For each moving average you'll be able to score Bullish, Bearish or Neutral for each of the conditions as mentioned in the filter above.

█ PLOTTING

• Standard: Symbols (EL, XS, ES, XL) Moving average lines are plotted with bearish, bullish and neutral zones, in the visuals section you can enable plotting by weight which will only show the parts of the moving average line to which weight is addressed.

• Conditional Settings: A larger icon appears if global conditions are met. For instance, with a Threshold(⥇) of 12, Signal Period (SP) of 3, and Scoring Condition (SC) set to "EVERY", a moving average signaling over two times in 3 candles (scoring 6 each) triggers a larger icon.

█ USAGE OF CONNECTABLE INDICATORS

■ Connectable chaining mechanism

Connectable indicators can be connected directly to the signal monitor, signal filter or strategy , or they can be daisy chained to each other while the last indicator in the chain connects to the signal monitor, signal filter or strategy. When using a signal filter you can chain the filter to the strategy input to make your chain complete.

• Direct chaining: Connect an indicator directly to the signal monitor, signal filter or strategy through the provided inputs (→).

• Daisy chaining: Connect indicators using the indicator input (→). The first in a daisy chain should have a flow (⌥) set to 'Indicator only'. Subsequent indicators use 'Both' to pass the previous weight. The final indicator connects to the signal monitor, signal filter, or strategy.

■ Set up this indicator with a signal filter and strategy

The indicator provides visual cues based on signal conditions. However, its weight system is best utilized when paired with a connectable signal filter, signal monitor, or strategy .

Let's connect the MA to a connectable signal filter and a strategy :

1. Load all relevant indicators

• Load MA / Connectable

• Load Signal filter / Connectable

• Load Strategy / Connectable

2. Signal Filter: Connect the MA to the Signal Filter

• Open the signal filter settings

• Choose one of the three input dropdowns (1→, 2→, 3→) and choose : MA / Connectable: Signal Connector

• Toggle the enable box before the connected input to enable the incoming signal

3. Signal Filter: Update the filter signals settings if needed

• The default settings of the filter enable EL (Enter Long), XL (Exit Long), ES (Enter Short) and XS (Exit Short).

4. Signal Filter: Update the weight threshold settings if needed

• All connectable indicators load by default with a score of 6 for each direction (EL, XL, ES, XS)

• By default, weight threshold (TH) is set at 5. This allows each occurrence to score, as the default score in each connectable indicator is 1 point above the threshold. Adjust to your liking.

5. Strategy: Connect the strategy to the signal filter in the strategy settings

• Select a strategy input → and select the Signal filter: Signal connector

6. Strategy: Enable filter compatible directions

• Set the signal mode of the strategy to a compatible direction with the signal filter.

Now that everything is connected, you'll notice green spikes in the signal filter representing long signals, and red spikes indicating short signals. Trades will also appear on the chart, complemented by a performance overview. Your journey is just beginning: delve into different scoring mechanisms, merge diverse connectable indicators, and craft unique chains. Instantly test your results and discover the potential of your configurations. Dive deep and enjoy the process!

█ BENEFITS

• Adaptable Modular Design: Arrange indicators in diverse structures via direct or daisy chaining, allowing tailored configurations to align with your analysis approach.

• Streamlined Backtesting: Simplify the iterative process of testing and adjusting combinations, facilitating a smoother exploration of potential setups.

• Intuitive Interface: Navigate TradingView with added ease. Integrate desired indicators, adjust settings, and establish alerts without delving into complex code.

• Signal Weight Precision: Leverage granular weight allocation among signals, offering a deeper layer of customization in strategy formulation.

• Advanced Signal Filtering: Define entry and exit conditions with more clarity, granting an added layer of strategy precision.

• Clear Visual Feedback: Distinct visual signals and cues enhance the readability of charts, promoting informed decision-making.

• Standardized Defaults: Indicators are equipped with universally recognized preset settings, ensuring consistency in initial setups across different types like momentum or volatility.

• Reliability: Our indicators are meticulously developed to prevent repainting. We strictly adhere to TradingView's coding conventions, ensuring our code is both performant and clean.

█ COMPATIBLE INDICATORS

Each indicator that incorporates our open-source 'azLibConnector' library and adheres to our conventions can be effortlessly integrated and used as detailed above.

For clarity and recognition within the TradingView platform, we append the suffix ' / Connectable' to every compatible indicator.

█ COMMON MISTAKES, CLARIFICATIONS AND TIPS

• Removing an indicator from a chain: Deleting a linked indicator and confirming the "remove study tree" alert will also remove all underlying indicators in the object tree. Before removing one, disconnect the adjacent indicators and move it to the object stack's bottom.

• Point systems: The azLibConnector provides 500 points for each direction (EL: Enter long, XL: Exit long, ES: Enter short, XS: Exit short) Remember this cap when devising a point structure.

• Flow misconfiguration: In daisy chains the first indicator should always have a flow (⌥) setting of 'indicator only' while other indicator should have a flow (⌥) setting of 'both'.

• Hide attributes: As connectable indicators send through quite some information you'll notice all the arguments are taking up some screenwidth and cause some visual clutter. You can disable arguments in Chart Settings / Status line.

• Layout and abbreviations: To maintain a consistent structure, we use abbreviations for each input. While this may initially seem complex, you'll quickly become familiar with them. Each abbreviation is also explained in the inline tooltips.

• Inputs: Connecting a connectable indicator directly to the strategy delivers the raw signal without a weight threshold, meaning every signal will trigger a trade.

█ A NOTE OF GRATITUDE

Through years of exploring TradingView and Pine Script, we've drawn immense inspiration from the community's knowledge and innovation. Thank you for being a constant source of motivation and insight.

█ RISK DISCLAIMER

Azullian's content, tools, scripts, articles, and educational offerings are presented purely for educational and informational uses. Please be aware that past performance should not be considered a predictor of future results.

KDJ / Connectable [Azullian]Enhance your analysis with our KDJ. Oscillate through buying and selling signals seamlessly, identifying potential reversals with accuracy.

This connectable KDJ indicator is part of an indicator system designed to help test, visualize and build strategy configurations without coding. Like all connectable indicators , it interacts through the TradingView input source, which serves as a signal connector to link indicators to each other. All connectable indicators send signal weight to the next node in the system until it reaches either a connectable signal monitor, signal filter and/or strategy.

█ UNIFORM SETTINGS AND A WAY OF WORK

Although connectable indicators may have specific weight scoring conditions, they all aim to follow a standardized general approach to weight scoring settings, as outlined below.

■ Connectable indicators - Settings

• 🗲 Energy: Energy applies an ATR multiplier to the plotted shapes on the chart. A higher value plots shapes farther away from the candle, enhancing visibility.

• ☼ Brightness: Brightness determines the opacity of the shape plotted on the chart, aiding visibility. Indicator weight also influences opacity.

• → Input: Use the input setting to specify a data source for the indicator. Here you can connect the indicator to other indicators.

• ⌥ Flow: Determine where you want to receive signals from:

○ Both: Weights from this indicator and the connected indicator will apply

○ Indicator only: Only weights from this indicator will apply

○ Input only: Only weights from the connected indicator will apply

• ⥅ Weight multiplier: Multiply all weights in the entire indicator by a given factor, useful for quickly testing different indicators in a granular setup.

• ⥇ Threshold: Set a threshold to indicate the minimum amount of weight it should receive to pass it through to the next indicator.

• ⥱ Limiter: Set a hard limit to the maximum amount of weight that can be fed through the indicator.

■ Connectable indicators - Weight scoring settings

▢ Weight scoring conditions

• SM – Signal mode: Enable specific conditions for weight scoring

○ All: All signals will be scored.

○ Entries only: Only entries will score.

○ Exits only: Only exits will score.

○ Entries & exits: Both entries and exits will score.

○ Zone: Continuous scoring for each candle within the zone.

• SP – Signal period: Defines a range of candles within which a signal can score.

• SC - Signal count: Specifies the number of bars to retrospectively examine and score.

○ Single: Score for a single occurrence

○ All occurrences: Score for all occurrences

○ Single + Threshold: Score for single occurrences within the signal period (SP)

○ Every + Threshold: Score for all occurrences within the signal period (SP)

▢ Weight scoring direction

• ES: Enter Short weight

• XL: Exit long weight

• EL: Enter Long weight

• XS: Exit Short weight

▢ Weight scoring values

• Weights can hold either positive or negative scores. Positive weights enhance a particular trading direction, while negative weights diminish it.

█ KDJ - INDICATOR SETTINGS

■ Main settings

• Enable/Disable Indicator: Toggle the entire indicator on or off.

• S - Source: Choose an alternative data source for the KDJ calculation.

• T - Timeframe: Select an alternative timeframe for the KDJ calculation.

• P - Period: Define the number of bars or periods used in the KDJ calculation.

• SL - Signal line: Adjust the smoothing factor for the KDJ's J line. This not only offers clearer buy/sell cues by reducing market noise but also determines the precise points for potential crossovers and crossunders.

■ Scoring functionality

• The KDJ scores long entries when the J line crosses over the signal (SL) line.

• The KDJ scores long exits when the J line crosses under the signal (SL) line after a prior crossover.

• The KDJ scores long zones the entire time the J line is above the signal (SL) line.

• The KDJ scores short entries when the J line crosses under the signal (SL) line.

• The KDJ scores short exits when the J line crosses over the signal (SL) line after a prior crossunder.

• The KDJ scores short zones the entire time the J line is below the signal (SL) line.

█ PLOTTING

• Standard: Symbols (EL, XS, ES, XL) appear relative to candles based on set conditions. Their opacity and position vary with weight.

• Conditional Settings: A larger icon appears if global conditions are met. For instance, with a Threshold(⥇) of 12, Signal Period (SP) of 3, and Scoring Condition (SC) set to "EVERY", an KDJ signaling over two times in 3 candles (scoring 6 each) triggers a larger icon.

█ USAGE OF CONNECTABLE INDICATORS

■ Connectable chaining mechanism

Connectable indicators can be connected directly to the signal monitor, signal filter or strategy , or they can be daisy chained to each other while the last indicator in the chain connects to the signal monitor, signal filter or strategy. When using a signal filter you can chain the filter to the strategy input to make your chain complete.

• Direct chaining: Connect an indicator directly to the signal monitor, signal filter or strategy through the provided inputs (→).

• Daisy chaining: Connect indicators using the indicator input (→). The first in a daisy chain should have a flow (⌥) set to 'Indicator only'. Subsequent indicators use 'Both' to pass the previous weight. The final indicator connects to the signal monitor, signal filter, or strategy.

■ Set up this indicator with a signal filter and strategy

The indicator provides visual cues based on signal conditions. However, its weight system is best utilized when paired with a connectable signal filter, signal monitor, or strategy .

Let's connect the KDJ to a connectable signal filter and a strategy :

1. Load all relevant indicators

• Load KDJ / Connectable

• Load Signal filter / Connectable

• Load Strategy / Connectable

2. Signal Filter: Connect the KDJ to the Signal Filter

• Open the signal filter settings

• Choose one of the three input dropdowns (1→, 2→, 3→) and choose : KDJ / Connectable: Signal Connector

• Toggle the enable box before the connected input to enable the incoming signal

3. Signal Filter: Update the filter signals settings if needed

• The default settings of the filter enable EL (Enter Long), XL (Exit Long), ES (Enter Short) and XS (Exit Short).

4. Signal Filter: Update the weight threshold settings if needed

• All connectable indicators load by default with a score of 6 for each direction (EL, XL, ES, XS)

• By default, weight threshold (TH) is set at 5. This allows each occurrence to score, as the default score in each connectable indicator is 1 point above the threshold. Adjust to your liking.

5. Strategy: Connect the strategy to the signal filter in the strategy settings

• Select a strategy input → and select the Signal filter: Signal connector

6. Strategy: Enable filter compatible directions

• Set the signal mode of the strategy to a compatible direction with the signal filter.

Now that everything is connected, you'll notice green spikes in the signal filter representing long signals, and red spikes indicating short signals. Trades will also appear on the chart, complemented by a performance overview. Your journey is just beginning: delve into different scoring mechanisms, merge diverse connectable indicators, and craft unique chains. Instantly test your results and discover the potential of your configurations. Dive deep and enjoy the process!

█ BENEFITS

• Adaptable Modular Design: Arrange indicators in diverse structures via direct or daisy chaining, allowing tailored configurations to align with your analysis approach.

• Streamlined Backtesting: Simplify the iterative process of testing and adjusting combinations, facilitating a smoother exploration of potential setups.

• Intuitive Interface: Navigate TradingView with added ease. Integrate desired indicators, adjust settings, and establish alerts without delving into complex code.

• Signal Weight Precision: Leverage granular weight allocation among signals, offering a deeper layer of customization in strategy formulation.

• Advanced Signal Filtering: Define entry and exit conditions with more clarity, granting an added layer of strategy precision.

• Clear Visual Feedback: Distinct visual signals and cues enhance the readability of charts, promoting informed decision-making.

• Standardized Defaults: Indicators are equipped with universally recognized preset settings, ensuring consistency in initial setups across different types like momentum or volatility.

• Reliability: Our indicators are meticulously developed to prevent repainting. We strictly adhere to TradingView's coding conventions, ensuring our code is both performant and clean.

█ COMPATIBLE INDICATORS

Each indicator that incorporates our open-source 'azLibConnector' library and adheres to our conventions can be effortlessly integrated and used as detailed above.

For clarity and recognition within the TradingView platform, we append the suffix ' / Connectable' to every compatible indicator.

█ COMMON MISTAKES, CLARIFICATIONS AND TIPS

• Removing an indicator from a chain: Deleting a linked indicator and confirming the "remove study tree" alert will also remove all underlying indicators in the object tree. Before removing one, disconnect the adjacent indicators and move it to the object stack's bottom.

• Point systems: The azLibConnector provides 500 points for each direction (EL: Enter long, XL: Exit long, ES: Enter short, XS: Exit short) Remember this cap when devising a point structure.

• Flow misconfiguration: In daisy chains the first indicator should always have a flow (⌥) setting of 'indicator only' while other indicator should have a flow (⌥) setting of 'both'.

• Hide attributes: As connectable indicators send through quite some information you'll notice all the arguments are taking up some screenwidth and cause some visual clutter. You can disable arguments in Chart Settings / Status line.

• Layout and abbreviations: To maintain a consistent structure, we use abbreviations for each input. While this may initially seem complex, you'll quickly become familiar with them. Each abbreviation is also explained in the inline tooltips.

• Inputs: Connecting a connectable indicator directly to the strategy delivers the raw signal without a weight threshold, meaning every signal will trigger a trade.

█ A NOTE OF GRATITUDE

Through years of exploring TradingView and Pine Script, we've drawn immense inspiration from the community's knowledge and innovation. Thank you for being a constant source of motivation and insight.

█ RISK DISCLAIMER

Azullian's content, tools, scripts, articles, and educational offerings are presented purely for educational and informational uses. Please be aware that past performance should not be considered a predictor of future results.

Donchian channels / Connectable [Azullian]Refine your breakout trading techniques with Donchian Channels. Accurately pinpoint significant highs and lows, enhancing your capacity to detect and react to key market movements.

This connectable Donchian channels indicator is part of an indicator system designed to help test, visualize and build strategy configurations without coding. Like all connectable indicators , it interacts through the TradingView input source, which serves as a signal connector to link indicators to each other. All connectable indicators send signal weight to the next node in the system until it reaches either a connectable signal monitor, signal filter and/or strategy.

█ UNIFORM SETTINGS AND A WAY OF WORK

Although connectable indicators may have specific weight scoring conditions, they all aim to follow a standardized general approach to weight scoring settings, as outlined below.

■ Connectable indicators - Settings

• 🗲 Energy: Energy applies an ATR multiplier to the plotted shapes on the chart. A higher value plots shapes farther away from the candle, enhancing visibility.

• ☼ Brightness: Brightness determines the opacity of the shape plotted on the chart, aiding visibility. Indicator weight also influences opacity.

• → Input: Use the input setting to specify a data source for the indicator. Here you can connect the indicator to other indicators.

• ⌥ Flow: Determine where you want to receive signals from:

○ Both: Weights from this indicator and the connected indicator will apply

○ Indicator only: Only weights from this indicator will apply

○ Input only: Only weights from the connected indicator will apply

• ⥅ Weight multiplier: Multiply all weights in the entire indicator by a given factor, useful for quickly testing different indicators in a granular setup.

• ⥇ Threshold: Set a threshold to indicate the minimum amount of weight it should receive to pass it through to the next indicator.

• ⥱ Limiter: Set a hard limit to the maximum amount of weight that can be fed through the indicator.

■ Connectable indicators - Weight scoring settings

▢ Weight scoring conditions

• SM – Signal mode: Enable specific conditions for weight scoring

○ All: All signals will be scored.

○ Entries only: Only entries will score

○ Exits only: Only exits will score.

○ Entries & exits: Both entries and exits will score.

○ Zone: Continuous scoring for each candle within the zone.

• SP – Signal period: Defines a range of candles within which a signal can score.

• SC - Signal count: Specifies the number of bars to retrospectively examine and score.

○ Single: Score for a single occurrence

○ All occurrences: Score for all occurrences

○ Single + Threshold: Score for single occurrences within the signal period (SP)

○ Every + Threshold: Score for all occurrences within the signal period (SP)

▢ Weight scoring direction

• ES: Enter Short weight

• XL: Exit long weight

• EL: Enter Long weight

• XS: Exit Short weight

▢ Weight scoring values

• Weights can hold either positive or negative scores. Positive weights enhance a particular trading direction, while negative weights diminish it.

█ Donchian channels - INDICATOR SETTINGS

■ Main settings

• Enable/Disable Indicator: Toggle the entire indicator on or off.

• S - Source: Choose an alternative data source for the Donchian channels calculation.

• T - Timeframe: Select an alternative timeframe for the Donchian channels calculation.

• LE - Length: Determine the period the Donchian channels are calculated on

• Enable/Disable plotting: Toggle the plotting of the Donchian channels

• U: Choose a color for the upper band

• B: Choose a color for the basis

• L: Choose a color for the lower band

• BG: Choose a color for Donchian channels background

■ Scoring functionality

• The Donchian channels score long entries when the current low price is equal to lower band.

• The Donchian channels score long exits when the current high price is equal to the upper band.

• The Donchian channels score long zones the entire time the current low price is equal to the lower band.

• The Donchian channels score short entries when the current high is equal to the upper band.

• The Donchian channels score short exits when the current low is equal to the lower band.

• The Donchian channels score short zones the entire time the current high price is equal to the upper band.

█ PLOTTING

• Standard: Symbols (EL, XS, ES, XL) appear relative to candles based on set conditions. Their opacity and position vary with weight.

• Conditional Settings: A larger icon appears if global conditions are met. For instance, with a Threshold(⥇) of 12, Signal Period (SP) of 3, and Scoring Condition (SC) set to "EVERY", a Donchian channels signaling over two times in 3 candles (scoring 6 each) triggers a larger icon.

█ USAGE OF CONNECTABLE INDICATORS

■ Connectable chaining mechanism

Connectable indicators can be connected directly to the signal monitor, signal filter or strategy , or they can be daisy chained to each other while the last indicator in the chain connects to the signal monitor, signal filter or strategy. When using a signal filter you can chain the filter to the strategy input to make your chain complete.

• Direct chaining: Connect an indicator directly to the signal monitor, signal filter or strategy through the provided inputs (→).

• Daisy chaining: Connect indicators using the indicator input (→). The first in a daisy chain should have a flow (⌥) set to 'Indicator only'. Subsequent indicators use 'Both' to pass the previous weight. The final indicator connects to the signal monitor, signal filter, or strategy.

■ Set up this indicator with a signal filter and strategy

The indicator provides visual cues based on signal conditions. However, its weight system is best utilized when paired with a connectable signal filter, signal monitor, or strategy .

Let's connect the Donchian channels to a connectable signal filter and a strategy :

1. Load all relevant indicators

• Load Donchian channels / Connectable

• Load Signal filter / Connectable

• Load Strategy / Connectable

2. Signal Filter: Connect the Donchian channels to the Signal Filter

• Open the signal filter settings

• Choose one of the three input dropdowns (1→, 2→, 3→) and choose : Donchian channels / Connectable: Signal Connector

• Toggle the enable box before the connected input to enable the incoming signal

3. Signal Filter: Update the filter signals settings if needed

• The default settings of the filter enable EL (Enter Long), XL (Exit Long), ES (Enter Short) and XS (Exit Short).

4. Signal Filter: Update the weight threshold settings if needed

• All connectable indicators load by default with a score of 6 for each direction (EL, XL, ES, XS)

• By default, weight threshold (TH) is set at 5. This allows each occurrence to score, as the default score in each connectable indicator is 1 point above the threshold. Adjust to your liking.

5. Strategy: Connect the strategy to the signal filter in the strategy settings

• Select a strategy input → and select the Signal filter: Signal connector

6. Strategy: Enable filter compatible directions

• Set the signal mode of the strategy to a compatible direction with the signal filter.

Now that everything is connected, you'll notice green spikes in the signal filter representing long signals, and red spikes indicating short signals. Trades will also appear on the chart, complemented by a performance overview. Your journey is just beginning: delve into different scoring mechanisms, merge diverse connectable indicators, and craft unique chains. Instantly test your results and discover the potential of your configurations. Dive deep and enjoy the process!